Profit №_12_2023, decembrie 2023

№_12_2023, decembrie 2023

A "Young" Currency in a Challenging Environment: The case of the Moldovan Leu

On 29 November 2018, the Republic of Moldova (Moldova in this article) will celebrate the 25th anniversary of the birth of its currency. Despite being soon 24 year old, the Moldovan Leu (the Leu/Lei) is still a young currency, especially when compared to other currencies with hundreds of years in existence. Being young is not something very unusual. After all, the European Union's (EU) currency (EUR) in its present format is actually younger. What is indeed extraordinary in the case of the Leu is the very challenging environment in which it was born and has existed so far. Nowadays, it is common that every country endeavours to have its own currency as a sign of identity, sovereignty and finally of well-being. Moldova and its currency are no exceptions. In the history of humanity, the intrinsic link between people's lives and money goes back many centuries. In modern times, more and more people think that everything is about money. As Oscar Wilde, the famous British play writer, put it: "When I was young I thought that money was the most important thing in life; now that I am old I know that it is". There is a lot of truth in this saying and this is also valid for the case of the Leu.

"Young" Currency

Moldova became an independent state on 27 August 1991, in the aftermath of the Soviet Union's dissolution. Because of this and in a very complex geo-political environment, the story of its currency is an interesting case. Before its independence, Moldova, like all the other 14 republics of the former Soviet Union, had used the Soviet Rouble and then for a short period of time the Russian Rouble. Also, for a brief period of time after its independence, Moldova had printed its own "coupons" before taking the bold decision to introduce its own currency. This happened on 29 November 1993, when, with the support of the IMF, it put in circulation the Leu (the first banknotes were printed abroad, in France).  From an economic point of view, some conditions for a stable currency had been met in those days, such as the lack of any foreign debt, the economic potential of the agriculture sector and, of course, the Moldovans' will to have their own monetary signs. These premises were of major importance, but it should be noted that Moldova barely had any foreign currency reserves and had no gold holdings whatsoever at the time when this new currency was "born". In the dissolution process of the former Soviet Union, Moldova opted for "no share of the foreign debt, no share of the international assets". The starting point of "no foreign debt" was a major positive factor (although rapidly lost in the transition to a market economy), but the lack of any gold holdings has haunted the currency up to nowadays. Based on the good results in the implementation of reforms, the Leu managed to remain stable in the first 5 years of circulation. In November 1993, the first exchange rate for Leu was established administratively by the National Bank of Moldova (NBM) at 3.85 Lei/USD. By end-1994, the depreciation process was quite mild, at 4.27 Lei/USD, at 4.50 Lei/USD as of end-1995 and at 4.66 Lei/USD by the end-1997.

From an economic point of view, some conditions for a stable currency had been met in those days, such as the lack of any foreign debt, the economic potential of the agriculture sector and, of course, the Moldovans' will to have their own monetary signs. These premises were of major importance, but it should be noted that Moldova barely had any foreign currency reserves and had no gold holdings whatsoever at the time when this new currency was "born". In the dissolution process of the former Soviet Union, Moldova opted for "no share of the foreign debt, no share of the international assets". The starting point of "no foreign debt" was a major positive factor (although rapidly lost in the transition to a market economy), but the lack of any gold holdings has haunted the currency up to nowadays. Based on the good results in the implementation of reforms, the Leu managed to remain stable in the first 5 years of circulation. In November 1993, the first exchange rate for Leu was established administratively by the National Bank of Moldova (NBM) at 3.85 Lei/USD. By end-1994, the depreciation process was quite mild, at 4.27 Lei/USD, at 4.50 Lei/USD as of end-1995 and at 4.66 Lei/USD by the end-1997.

The economic potential of this country was quite good if compared to its geographic and human dimensions, but it was not used to the highest level. By the time of the introduction of its currency, Moldova had registered a sharp economic decline (-31% of GDP in 1994 and -3.2% in 1995, after four previous years of massive reductions of GDP during 1990-1993). Inflation was extremely high (1,283% in 1993 and 587% in 1994) and the state budget deficits were also very high (approximately 5-8% of GDP). Despite the so called zero option (no foreign debt, no external assets), Moldova's foreign debt started to accumulate at a rapid pace. The level of USD 700 million had been already reached by October 1996. By mid-1997, the same indicator had reached USD 1 billion, according to the figures published by the NBM. This represented 50% of the Moldovan GDP which was quite concerning. Moreover, over the next 20 years, the foreign debt would build up to a staggering level of USD 6.6 billion (EUR 6.25 billion) by end-2016. This was already equal to approximately 100% of GDP. Nevertheless, the foreign currency reserves evolved reasonably well under these circumstances.

Banking Sector, IFIs and International Ratings

The Moldovan banking sector, which was important for the introduction and evolution of the Leu, was quite different as compared to other countries in transition. Moldova inherited from the former Soviet Union's four branches of the former specialised banks, of which one for agriculture, one for industry, trade and services, one for financing the social sector and the last one for keeping the population's savings. The four entities rapidly adjusted to the new realities and became universal banks after 1991. This is the short narrative of the four largest banks of the country in the early days of the transition: Moldova-Agroindbank, Moldindconbank, Banca Socială (Social Bank) and Banca de Economii (Savings Bank) (the last two banks and Unibank entered into a liquidation process in 2015 (see Box)). In parallel, new private banks were established and started to develop.

In parallel, in August 1992, Moldova became a full member of the IMF and the World Bank Group. The memberships in these international financial institutions (IFIs) represented an important achievement for the new Moldovan authorities. These laid out the foundations for the new Moldovan currency which was to be issued one year after. During the initial years of the Leu's existence, the NBM conducted a very restrictive policy. The refinancing rates for commercial banks reached an unusual level of 377% in March 1994. The minimum reserves requirements for commercial banks were kept at very high levels (for instance, in 1994 at approximately 28%). The refinancing level was then relaxed to 19% in April 1996 and the minimum reserves requirements were reduced from 12% as of end-1995 to 8% by end-1996 More recently, it was fixed at 7.0% on 25 October 2017. Under these circumstances, Moldova accepted the provisions of Article VIII of the IMF Charter on 30 June 1995. The IMF members accepting these provisions undertake to abstain from the introduction of any restrictions regarding international payments and current account transfers and to eliminate any discriminatory practices on foreign currency regimes. This means, de facto, a current account currency convertibility. For capital account convertibility, the fulfilment of more requirements is needed first. In November 2016, Moldova signed a new program with the IMF for the amount of USD 178.7 million. The conditionality of this last program is rich, especially on the banking sector supervision and restructuring of this key sector. As of end-October 2017, an amount of USD 58.6 million was disbursed to Moldova.

In parallel, in August 1992, Moldova became a full member of the IMF and the World Bank Group. The memberships in these international financial institutions (IFIs) represented an important achievement for the new Moldovan authorities. These laid out the foundations for the new Moldovan currency which was to be issued one year after. During the initial years of the Leu's existence, the NBM conducted a very restrictive policy. The refinancing rates for commercial banks reached an unusual level of 377% in March 1994. The minimum reserves requirements for commercial banks were kept at very high levels (for instance, in 1994 at approximately 28%). The refinancing level was then relaxed to 19% in April 1996 and the minimum reserves requirements were reduced from 12% as of end-1995 to 8% by end-1996 More recently, it was fixed at 7.0% on 25 October 2017. Under these circumstances, Moldova accepted the provisions of Article VIII of the IMF Charter on 30 June 1995. The IMF members accepting these provisions undertake to abstain from the introduction of any restrictions regarding international payments and current account transfers and to eliminate any discriminatory practices on foreign currency regimes. This means, de facto, a current account currency convertibility. For capital account convertibility, the fulfilment of more requirements is needed first. In November 2016, Moldova signed a new program with the IMF for the amount of USD 178.7 million. The conditionality of this last program is rich, especially on the banking sector supervision and restructuring of this key sector. As of end-October 2017, an amount of USD 58.6 million was disbursed to Moldova.

In the first part of its transition, Moldova was a country which exemplarily implemented all the agreements concluded with the IMF and other IFIs, especially with regard to the credit level. Based on the good results in the implementation of reforms, Moldova succeeded in obtaining favourable quotes from reputable international agencies during the ‘90s, such as a very good rating from Moody's of Ba2 in 1996. However, this advantage has been lost due to the severe political, financial and banking developments during the last 3-5 years to date. For instance, a new recent quote from Moody's Investors Service was of only B3 on 13 January 2017 (with stable outlook) and this was possible only after a new agreement with the IMF.

Leu's Recent Developments

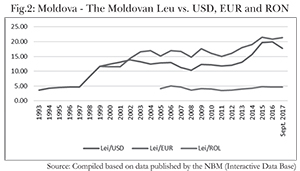

These were good achievements back in those days and it reflected as such in the relative stability of the Leu. However, the evolution of this new currency was to follow more dramatic developments in the coming years. First of all, a very steep depreciation followed the 1998 crisis, as presented below. The second one was to follow in 2014 (see Fig. 2). While the introduction and the trend of this "young" currency were good in the first part of its history, the current status of the currency is not so great, however. A strong economic recovery is now required to bring stability for the Leu. This implies the restructuring of large state owned companies which currently register losses or receive subsidies from the budget and the substantial increase in exports, including to the CIS countries. The land should be distributed to farmers and in turn the farmers should produce more organic foods for both the internal market and more so for export in EU and other international markets. Also, the strong control of the foreign debt should/must be a priority for the current Moldovan authorities. An adequate structure of the foreign debt is desirable, but realistically maybe Moldova is not in the position to juggle/choose amongst its creditors. It simply has not got enough borrowing capacity to be able to diversify the sources of its external financing. The latest loan granted by Romania, of EUR 150 million in three tranches, in October 2015 (fully disbursed by 27 September 2017) was more of an emergency loan extended by a friendly neighbouring country than a normal access to international capital markets.

The Moldovan foreign debt has had and will continue to have a material impact on the fate of the Leu. In addition, the debt accumulated by the companies established in Transnistria has been and will continue to be a topic of heated discussions in the Moldovan society, as the break-away unrecognized republic of Transnistria has been supported by the Russian Federation ever since Moldova's independence in 1991. As such, the question was and still is whether Moldova should pay for the debt resulting from the transactions of Transnistrian entities. Moldova has been and will continue to be externally vulnerable because of its almost total dependence on energy imports from the Russian Federation and other CIS countries. In the winter of 1996, Moldova was forced to introduce the "state of emergency" as the Russian Federation reduced its exports of oil, natural gas and energy. In more recent years, Moldova had another type of difficulties generated by restrictions and/or by the total prohibition of exports of some traditional products (wine, cognac, meat, vegetables, fruits etc.) on the Russian markets. This was supposedly done for phytosanitary reasons, but all external analysts of the Moldovan developments agree that the restrictions were mainly geo-politically motivated.

Remittances

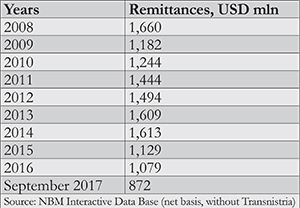

There has been and, for the foreseeable future, there will continue to be a direct correlation between the exchange rate of the Leu and the level of remittances (transfers of some one million of Moldovans working abroad). From this point of view, Moldova and its currency is an illustrative case of such a statement. Moldova received during the last 10 years, on annual basis, an average USD 1.3-1.4 billion from its citizens currently living and working in the Russian Federation, EU, USA, United Kingdom, Israel and many other countries. In some years, this represented up to 20% of the Moldovan GDP, but the large majority of this money is going for consumption/subsistence, which is not the best trend one can hope. As such, the exchange rate of the Leu is clearly related to the volume of remittances as presented below. The IFIs, including EBRD, granted free technical assistance to Moldova (and other CIS countries) for education of public at large on how to make such transfers via official channels (banks, money-transfer chains, etc.) and, even more, how to utilize such important resources for investments. The large transfers helped considerably the Leu to stay afloat, but if the total level of remittances will decline (as seem to be the tendency of the last years), the exchange rate of the Leu will clearly be negatively impacted. No doubts that pressure on the currency will continue without a solid stream of remittances. The ratio of consumption/investments will be also influential and the increase of the investment share will help supporting the Leu.

The IFIs, including EBRD, granted free technical assistance to Moldova (and other CIS countries) for education of public at large on how to make such transfers via official channels (banks, money-transfer chains, etc.) and, even more, how to utilize such important resources for investments. The large transfers helped considerably the Leu to stay afloat, but if the total level of remittances will decline (as seem to be the tendency of the last years), the exchange rate of the Leu will clearly be negatively impacted. No doubts that pressure on the currency will continue without a solid stream of remittances. The ratio of consumption/investments will be also influential and the increase of the investment share will help supporting the Leu.

Recent Evolutions in Banking Sector

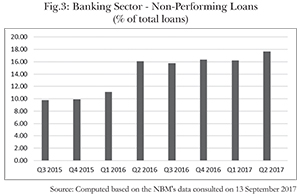

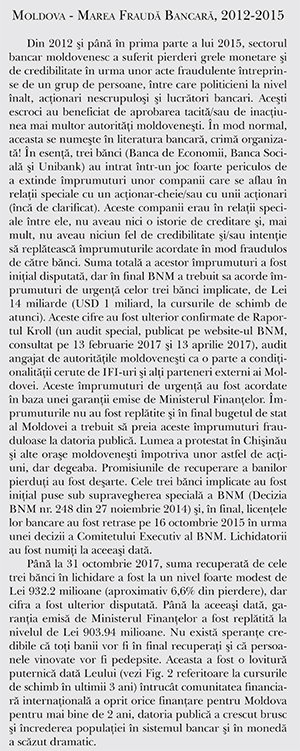

The status of the Leu, both internally and externally, has been under heavy pressure during the last 5 years. The supervision of the NBM up to end-March 2016 was weak. The banking sector was plagued by severe scandals, of which the so-called "the Moldovan laundromat" and the huge banking fraud (see Box) were the most damaging for the Leu. Regarding the first one, in summary, some Moldovan banks were involved in money laundering transactions involving Russian funds, Russian entities, commercial banks from Moldova, the Russian Federation, the Baltics and Moldovan state's legal entities/authorities (courts, prosecutors, bailiffs, public notaries, lawyers, etc.). According to independent analysts, some USD 20 billion (more recent figures put it at USD 22 billion) were "laundered" from the Russian Federation to off-shore jurisdictions in rather sophisticated schemes, described frequently by the Moldovan and international mass media. The Moldovan banks acted on these transactions as a commission fee-takers, based on a decision of a Moldovan court and under the order of a Moldovan bailiff. All these dubious transactions were automatically reported by the banks to the NBM and to the then Centre for Fighting Corruption and Combating Terrorism. Back in 2014, the Moldovan authorities asked their Russian counterparts about the origin of the money transferred from the Russian accounts with the Moldovan banks to Latvian banks and then to off-shore jurisdictions. The Russian Federation never responded. All these transactions had been implemented for years, up to May 2014, when the whole scheme became public. Many judges and bailiffs involved were arrested and many managers of the involved banks (and from the NBM) were fired/dismissed/arrested/had the banking administrator licences revoked. However, this was too little, too late! The damage was done and the Moldovan Leu entered into a continuous process of depreciation.  One collateral negative impact of money laundering and of the banking fraud toxic transactions was the unprecedented increase in non-performing loans in the Moldovan banking sector, as presented in Fig. 3 below. The sharp increase from 9.79% as of end-September 2015 to 16.31% as of end-2016 (and to 17.64% as of June 2017) was mainly caused by two key trends (one more negative than the other): a) the absolute increase in non-performing loans from Lei 3,877.24 million to Lei 5,669.86 million during this period which has to do with the state of the economy and with the economic attitude of a society traumatised by the banking fraud; and b) a more worrisome trend of decline in the total loans from Lei 39,613.06 million to Lei 34,761.27 million (increasing trends of non-performings were registered as of June 2017 as well). The second trend had a substantial impact on the economic growth of the country and hence on the recent weakness of the Moldovan Leu in a turbulent regional geo-political context.

One collateral negative impact of money laundering and of the banking fraud toxic transactions was the unprecedented increase in non-performing loans in the Moldovan banking sector, as presented in Fig. 3 below. The sharp increase from 9.79% as of end-September 2015 to 16.31% as of end-2016 (and to 17.64% as of June 2017) was mainly caused by two key trends (one more negative than the other): a) the absolute increase in non-performing loans from Lei 3,877.24 million to Lei 5,669.86 million during this period which has to do with the state of the economy and with the economic attitude of a society traumatised by the banking fraud; and b) a more worrisome trend of decline in the total loans from Lei 39,613.06 million to Lei 34,761.27 million (increasing trends of non-performings were registered as of June 2017 as well). The second trend had a substantial impact on the economic growth of the country and hence on the recent weakness of the Moldovan Leu in a turbulent regional geo-political context.

In addition, another serious problem of the Moldovan banks was related to the very existence of non-transparent shareholders in almost all the banks in the country, apart from a few medium and small banks with reputable foreign shareholders. This led to or allowed "raiders' attacks" on the shares of some of the largest banks, such as Moldova-Agroindbank and Victoria Bank and of some insurance companies. In this respect, the supervision of the National Bank kept failing until a new Governor was appointed by the Moldovan Parliament (Decision no. 31 dated 11 March 2016 with the starting date of 11 April 2016) when measures to correct this unacceptable situation started to be implemented. This issue is not over yet and the (already registered) unfavourable impact on the Leu will continue for a while.

Under such circumstances, corroborated with the second large scandal presented above, the currency sharply depreciated to 20.87 lei/EUR and to 20.04 lei/USD, respectively, as of end-2016. As of 30 September 2017, the Leu was quoted at 20.74 lei/EUR. During 2015-2016, the level of 22.00 lei/EUR was exceeded which shows the fragility of a young currency unable to weather the extreme conditions derived from scandals, frauds and a struggling economy of a country at the crossroads. An incipient and fragile appreciation trend was experienced by the Leu in the first half of 2017 (mainly versus USD), appreciation related to the new external financing ensured by Moldova from IFIs and the EU. Fighting Corruption

Fighting Corruption

There is a clear agreement between the market analysts that the level of corruption is a crucial factor determining the fate of any currency. This is true for Moldova as well. However, fighting corruption in this country is more a national "show" on which mass media makes audience. The actual results are pretty modest, if any. There is a need of a strong political will to fight corruption and it is obvious that this lacks in the case of Moldova. In turn, this has determined and will continue to have a negative impact on the fate of the Leu. The main issue here is that the political field is the key generator of corruption and hence the lack of the political will to eradicate this plague. The state authorities empowered by the law to fight corruption are "controlled" by the political decision-makers and their actions and consequently their results are accordingly weak.

In the case of Moldova (and of other countries too), the fight against corruption should start with the education in the schools and universities. This is a process which may take generations, but finally it will pay off. The civic society, including trade unions (see the results of Kiev Conference in September 2017), and mass media should also play a key role in fighting corruption. The investigative journalism should be cultivated and supported so that the journalists can bring undoubtful proofs against those corrupted. All state authorised bodies (such as the Office of General Prosecutor, the Anti-Corruption National Centre, special intelligence services, courts, etc.) should be enforced and taken out of control of oligarchs. Their international cooperation should be promoted as it should be the exchange of information with international powerful organisations specialised in this field. Specific for Moldova, the ban of the shareholders registered in fiscal paradises or in non-cooperant jurisdictions should have been done long time ago. Though it is not too late if there is a will in this respect as much more is required for the image of the country and for the stability of the Leu's exchange rate. Finally, the law in Moldova should be improved to apply severe penalties against those who are finally proved as corrupt. The confiscation by the Moldovan state of the proceeds resulting from fraudulent transactions will have a positive impact on the state budget equilibrium (the state cash deficit was of 2.1% of GDP in 2016 and is projected to increase to 3.7% for 2017) and finally on the status of the Leu, both domestically and externally.

Instead of Conclusions

There are no easy conclusions to this article as any such conclusions could be sensitive in the present geo-political environment from the region. By the way of concluding, though, it would be fair to say that the short history of Moldova's transition to a market economy, of its "young" Leu and, even more so, of its present status are just mere reflections of the economy, domestic monetary and fiscal policies, international context and, more importantly, the population's attitude towards the Leu. Moreover, one clear red-line could be easily derived: a currency is strong(er) as long as it is supported by a healthy and robust economy. Building such an economy should be a national goal for Moldova. Adherence to it by the whole community, local and central authorities, commercial banks, central bank, government and politicians is crucial. Without all moving together in the same direction and in a well-coordinated manner, the Leu may not flourish. Moldova's current good potential is there waiting to be harnessed. The country signed a Deep and Comprehensive Free Trade Agreement (DCFTA) with the EU in June 2014 (with full effect from 1 July 2016), but the benefits are still to be fully utilized. In this endeavour, Moldova could be helped by the EU, IMF, the World Bank and other major IFIs. Meanwhile, let us remind ourselves that a strong currency should be supported by a strong economy (and not vice-versa as implied by some Moldovan authorities in October 2017). Moldova and its "young" Leu cannot escape this fundamental truth of economics.■

_______________________________________________________________________

Alex M. Tanase is an Independent Consultant and Former Associate Director, Senior Banker at EBRD and former IMF Advisor.

The assessments and views expressed are not those of the IMF and/or the World Bank and/or NBM and/or the EBRD and/or indeed of any other institution quoted. The assessment and data are based on information as of end-September 2017.

Adauga-ţi comentariu