Profit №_12_2023, decembrie 2023

№_12_2023, decembrie 2023

Romania and Moldova: The evolution of the exchange rate as an instrument of economic policy

When the current difficult period, generated by the COVID-19 pandemic is over, Romania, as an European Union (EU) country, and the Republic of Moldova (Moldova in this article), should focus on proper control of their macroeconomic equilibria to relaunch economic growth. In the case of Romania, some key elements have already been presented in an article published by Emerging Europe on December 14, 2020. However, the subject deserves a separate analysis.

A polarised political scene

The current pandemic crisis has strongly hit almost every country on the globe, including the former socialist countries in transition or those which are currently treated as emerging markets. Despite this, 2020 was a year of elections (local, presidential and/or parliamentary) in many transition countries such as Croatia, Serbia, North Macedonia, Romania, Moldova, Belarus etc. In addition, numerous protests have polarized the political scene in various regions. In all of these countries, banking issues were not among the highest priorities for Governments, academia, analysts and/or practical decision-makers. With interest rates at their historical lowest levels or even negative, the central banks in many transition countries struggled to alleviate the costs associated with the COVID-19 pandemic and the sharp decline of economic activities. No wonder that under such circumstances, the practical issues related to exchange rates took a secondary place. Yet, their implications should not be underestimated. To underline the importance of this instrument, the US Department of Treasury developed a monitoring list of those countries deemed to manipulate their exchange rates. As of December 2020, Switzerland, Vietnam, India, Thailand, Taiwan, China, Japan, Korea, Germany, Italy, Singapore and Malaysia were on the list of the alleged manipulators.

The importance of the exchange rate instrument in the measurement of the efficiency of economic activity for transition countries cannot be emphasised more. The central banks of the developed countries were, of course, more experienced and had more freedom in using their currencies’ exchange rates, as required by market developments, as compared to the former planned economies. Using them to stimulate their exports and to reduce the trade deficits and consequently current account deficits was just normal. But in the cases of the former socialist countries, everything was much more complicated. This group of states started their transition to markets economies more than 30 years ago, after years and years of rigid (″planned″) domestic prices which inevitably rendered the exchange rates in these countries, during extensive periods before transition, as almost useless (or worse) to turn it into macroeconomic instruments.

Romania - dramatic evolutions

1. Misalignments under socialist times

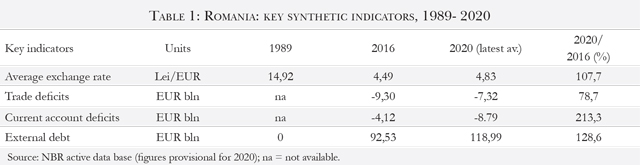

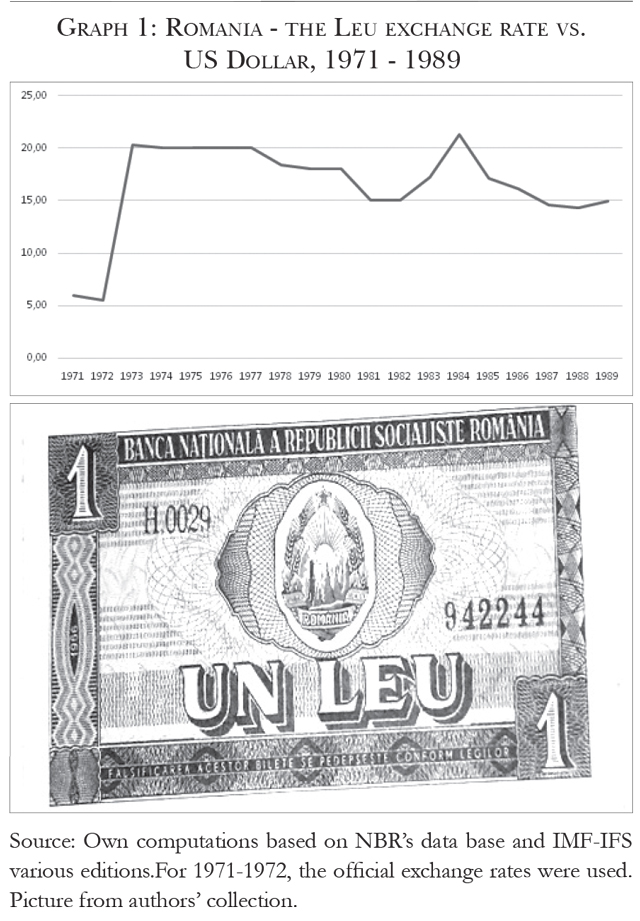

The case of Romania was no different. On 15 December 2020, Romania marked 48 years of membership of the International Monetary Fund (IMF) and the World Bank Group. It was the second socialist country (after the former Yugoslavia) to become a member of such prestigious institutions. However, the anniversary took place in special circumstances. The last three decades of the socialist years were those of misalignment of the old Romanian Leu’s exchange rate to the US Dollar and/or other currencies in use in those days. In practice, the then Romanian authorities tried many times, mainly based on ideological reasons and especially after 1985, to show the strength of their socialist achievements through “strong” Leu exchange rates. Even the name of the exchange rate and its role was changed many times (official exchange rate, non-commercial exchange rate, commercial exchange rate, etc.) despite the IMF membership and the obligation to put its house in order regarding the currency exchange rates.

A ″representative″ exchange rate was agreed with the IMF in 1973 at the level of 14.38 Lei to the one US Dollar. Since then, both commercial and non-commercial exchange rates started to be properly reported and monitored. However, the key exchange rate, a unified commercial rate at 15.00 Lei/USD (unified commercial rate) continued to significantly diverge from the actual cost of producing goods and services for which one US Dollar was obtained in export transactions. Large disparities were registered on the imports side too as many raw materials imported by Romania had fixed domestic prices. This made the exchange rate a misleading instrument for the efficiency of foreign trade and services.

2. New realities

Many things started to change after the events of December 1989. Amongst the key ones was the recognition that the Leu’s exchange rate should reflect the new realities and, therefore, be freely determined by the market, without interventions. All that was well and good, except that the fluctuations of the exchange rate were very large (to put it mildly) and the depreciation-inflation-depreciation spiral became a common reality.

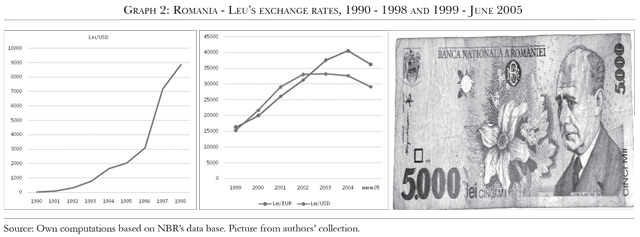

The Leu took a very sinuous road from 21.56 Lei/USD in 1990 to 8,875.55 Lei/USD in 1998, and from that level to 29,136.55 Lei/USD for the six months to June 2005, when the Leu’s re-denomination took place. The euro started to be quoted in 1999 with an average exchange rate of 16,295.57 Lei/EUR for that year, which sharply depreciated to an average of 36,234.38 Lei/EUR before re-denomination. What an extraordinary journey!

It would be quite difficult to say that the Leu’s exchange rate played its role as a proper measure for the efficiency of Romania’s external trade during the first 15 years of transition to a market economy. Under such circumstance, the National Bank of Romania (NBR) did not have many choices. The logical solution was to proceed with a re-denomination on 1 July 2005, when 10,000 old Lei became one Leu. This was in all but name a monetary stabilisation of the Leu similar to that implemented in 1947 (admittedly in very different historical conditions).

3. The calm after re-denomination

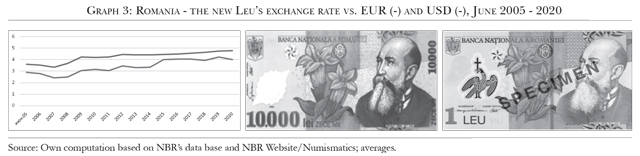

After 2005, Romania benefited from a very favourable external context, being admitted in 2004 to the North Atlantic Treaty Organization (NATO) and becoming a full EU member on 1 January 2007. The Leu’s exchange rate suffered from high depreciation in the aftermath of the financial crisis of 2008, but these depreciations were not translated in export increases as expected. The current account deficits continued to widen and as such a large foreign debt started to accumulate.

There are multiple reasons for such an ″abnormal″ economic case: decrease of internal output, historically large emigration of the young labour force, focus on consumption (mainly of imported goods), large spending on foreign holidays and services, non-stimulatory exchange rates applied to remittances and many other similar ill-advised economic policies.

On top of all that, significant political drawbacks were registered, corruption and mismanagement of public funds continued, all of which finally put pressure on the exchange rate and its designated role. Despite all of this, over the last five years, the Leu’s exchange rates have been much better managed, which has contributed to relative stability of the currency.

4. Debt piling up

However, the Leu’s fundamental support from strong economic developments has been and is still missing (exacerbated, inter alia, by the 2020 pandemic) and, consequently, the foreign debt reached 119 billion euro at the end of October 2020. If not strictly monitored, the sizable external debt, estimated at over 57% of GDP, could easily destroy the last five years of achievements in this respect. It is true that during the pandemic crisis all nations continued to borrow internally and externally as well. All hopes are now related to the successful vaccination of large categories of the population.

As and when the pandemic crisis is over, Romania, like many other EU countries, should focus on proper control of its macroeconomic equilibria and other measures (absorption of allocated EU funds, implementation of infrastructure projects, stimulation of savings, through adequate interest rates as an internal source of capital and the like) to relaunch economic growth. This should be an immediate priority for the new Government, which was appointed on 23 December 2020, formed following parliamentary elections earlier that month.

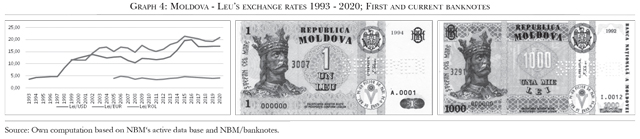

Moldova - from former URSS to European family

1. The birth of a new currency

Moldova became member of the IMF and World Bank Group on 12 August 1992, one year after declaring its independence in 1991. One year later, on 29 November 1993, Moldova took a much-needed decision to introduce its own currency to replace the former Soviet and Russian Ruble. The initial rate of 3.65 MDL/USD was an administrative one, but it was close enough to its equilibrium level. Therefore, its exchange rate remained relatively stable in the first years after its introduction, but the Leu suffered its first heavy blow in the aftermath of the 1998 crisis. More strong hits were to come after 2008 crisis and the most recent one after the largest fraud in the history of Moldova of $1 billion stolen from three banks (Banca de Economii, Banca Socială and Unibank – all of them declared bankrupt in 2016 and currently in liquidation).

2. The evolution of the Moldovan Leu’s exchange rates

A detailed view of exchange rates over almost three decades (see Graph 4) shows that the fate of the Moldovan Leu was intrinsically linked with both external and internal factors. For instance, the 1998 and 2008 international financial crisis and the large banking fraud caused significant currency depreciation. One could immediately ask if such large depreciations produced significant increases of the Moldovan exports and/or sizable reductions of imports. The answer is no.

The classical correlation of depreciation/export increase/import decrease did not work as many other factors were at play. The embargo of the Moldovan wines exports on the Russian markets for many years (determined by rather political reasons) is one of the most conclusive examples. At the same time, any other reasons contributed, such as geopolitical factors in the region, cut off external financing, a decline of remittances during some periods of time, psychological negative impact etc.

3. Foreign debt piling up

Like in the case of many other countries, the external debt of Moldova grew at a fast pace since the country’s independence. Moldova started its transition in 1991 with zero foreign debt and by the end-September 2020 it accumulated an impressive foreign debt of $7.95 billion, which represents 67.3% of GDP (see Table 2).

It is very likely that Moldova's external debt will continue to grow, as its economic recovery will require adequate financing. To control this increasing trend, everything must be exercised with great caution. Now, Moldova is in a favourable position to restart its economic growth. A new reformed-oriented President took office on 24 December 2020. Thus, so far there are clear commitments from Moldova’s external partners and international financial institutions to support the country’s many reforms neglected for a long period of time due to political environment and/or to alleviate the negative impact of the current pandemic. A new Government will be appointed early 2021. Accessing external financial support, stimulating the foreign currency remittances from a strong Moldovan community of working abroad (estimated to more than one million persons sending home by November 2020 – $1.3 billion) combined with domestic efforts will be crucial in the next immediate period. If there will be political will and a favourable external context, this could be the answer (or at least a part of it) to bring Moldova into the fold of the European family.■

__________________________________________________________________________________________

Alexandru M. TĂNASE is an independent consultant and former Associate Director, Senior Banker at the EBRD and former IMF Advisor. Mihai RĂDOI is a Director of a specialised Investment Fund focused on Eastern Europe and former Executive Director of Anglo-Romanian Bank, London and previously of the BFR Bank, Paris. These are personal views of the authors. The assessments and views expressed are not those of the EBRD and/or of the IMF and/or of the NBR and/or of any other institution quoted. The assessment and data are based on information as of December 2020.

__________________________________________________________________________________________

Adauga-ţi comentariu