Profit №_12_2023, decembrie 2023

№_12_2023, decembrie 2023

Purchasing power parity in transition

The issue of the exchange rates has been, is and will continue to be a very complex topic of high interest due to major implications which they have in economic, banking, entrepreneurial sectors and/or personal life of ordinary peoples. The value reports between various currencies are nowadays in the remit of central and commercial banks and of stock exchanges as well. The way in which various currencies are evolving as compared to others seems in most cases to be chaotic and for sure almost impossible to predict. This very simple fact gives to the exchange rate a true mystic aura.

Solid Theoretical Foundations - Persistent Practical Issues

World-wide well known economists, international financial organisations, stock exchanges, analysts of most varied orientations and practices, etc. have tried during many centuries to discover the essence of formation mechanisms and in particular the way in which these exchange rates evolved. Not all of them were successful due to the complexity of this almost "impossible" task.

First of all, the equilibrium exchange rate raised the issue of the adequate corresponding level which have to be reached and/or maintained on a daily basis and especially in the case of those countries which prepare their own currencies to become fully convertible (both for current account and for capital account as well). Apparently only, the easiest answer to this issue was given a long time ago when a concept was in fashion during the interwar period, namely the Purchasing Power Parity (PPP) (see G. Cassel, La monnaie et le change après 1914, Girard, Paris, 1923). The issue seemed resolved, but later on it was proven that it was just an illusion.

In practice, the use of PPP by those countries in transition from centrally planned economies to market ones was and continues to be almost impossible. The simple fact that most of these countries had their domestic prices distorted during long periods of time (decades in most of the cases) was the first and most insurmountable obstacle in finding the correct equilibrium level for their exchange rate.

Then, second, the former CMEA (Council for Mutual Economic Assistance (CMEA), disbanded after 1991) countries had their external prices for their intra-CMEA trade distorted as well as in the case of the internal ones. This was all the more important as the weight of the intra-CMEA trade denominated in the former "transferable roubles" (CMEA account currency, artificially over-valued, abandoned after dis-establishment of CMEA) was higher.

The 1991 edition of the IMF publication World Economic Outlook showed that in 1990 between 25 and 40% of the former Czechoslovakia, Hungary, Poland, Romania and the former Soviet Union's exports went to partners from the former CMEA countries. The case of Bulgaria, which had this weight at some 70%, deserves a special mention.

Under such circumstances, many economists and economic decision-makers from the transition countries (and from the developed ones) realised soon that finding the correct answer regarding the level of exchange rate will take some time. Meanwhile, some policies were implemented to introduce flexible exchange rates, but large fluctuations had appeared immediately. When and how this process will stabilize remained an open question for a long period of time.

Currently, there are doubts that, in the case of transition countries, the exchange rate changes have the impact presented and proven by the economic theory, namely that the depreciation of a certain currency helps under certain conditions growth of exports and reduction of imports. What was needed to be undertaken by these countries, as a matter of priority, was the elimination of the large "non-alignments" shown by the exchange rates and internal prices. Poland's plans for a guided, controlled and as much as possible uniform depreciation of the zloty (announced on 15 October 1991) were illustrative by themselves for the starting of the transition era on what was needed for the alignment of the nominal exchange rates to the equilibrium ones.

Meanwhile, Poland was the only country who succeeded to finish the transition process by September 2018, from which date this country was re-classified in the international statistics and included in the group of OECD countries. For many other ones, the transition process continues.

The case of the Soviet rouble was also very illustrative one from this point of view. Looking back, it is known that the first steps to depreciate an over-valued rouble were taken at the beginning of ‘90s. The financial markets and analysts were shocked when the former Soviet Union accepted that the rouble should be devalued at the level of 6 - 10 roubles/dollar, especially that such things had happened after decades of rigid and over-valued exchange rates. This was followed by very convoluted periods in the rouble history, which was already quoted at 5,569 roubles/dollar by the end-1996. Like in the case of other countries (Romania, Ukraine, etc.), Russia re-denominated its rouble in 2008 by cutting three zeroes and change of its code.

Currently, the Russian Federation rouble is quoted by the Central Bank at 67.1920 roubles/dollar (15 January 2019), as compared to 33.2386 roubles/dollar five years ago. Even so, the issue of the equilibrium exchange rate remains open. It is very likely that this one will be solved only when the political and social climate, on the one hand, and the economic development, on the other hand, will settle on a normal track. On a more general plan, this situation is valid for the large majority of the transition countries. A case-by-case analysis is required in an economic, political and social life of extreme diversity.

The Theory and Practice of Leu's Forecast Romania's case

Despite the fact that during Romania's transition to a market economy the issue of the exchange rate was one of the most debated topics by the Romanian mass-media, the matter was insufficiently researched from the theoretical point of view. The Romanian economic literature does not currently have an exhaustive theoretical analysis of the PPP concept.

Theoreticians and those practicing were not able to respond with any particular accuracy to the question: which would have been the level of the exchange rate scientifically determined? This was the cause of some very dangerous cases in Romania during the ‘90s when the speculative opinions were the most in fashion. It was quite clear that those making such statements were not in the possession of any scientific computations.

The National Bank of Romania (NBR) was forced many times to publically deny such statements. Unfortunately, even NBR was not able/did not offer a scientific foundation of the exchange rate and/or of its evolution on short or medium term. The negative consequences of these true games of "forecast- denials" were evident. The Leu's exchange rate did not follow any economic law and the start of the "rush for dollars" was inevitable as the dollar was the only refuge currency which was still fully trusted. The so called "Dollarisation" (and later on the tendency to save/borrow in Euro) of many countries' economies (Romania, Bulgaria, Serbia, Macedonia (to be renamed soon as North Macedonia), Republic of Moldova, Hungary, etc.) was the key feature as reflected in the structure of the population's monetary holdings and in the borrowing preferences of the companies and/or of the population from the commercial banks.

Under these circumstances, the type of questions such as: how much should be an actual exchange rate? or: how will the exchange rate evolve in the future or on a 2-3 year horizon? remained unanswered.

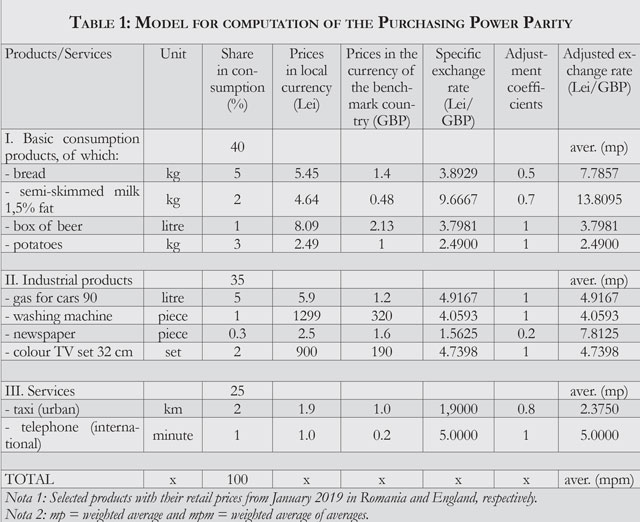

Without any ambition to offer a definitive answer to the first question, namely how much should be the actual exchange rate, we have suggested back in 1997 a model which should have been studied by the people in charge from the central bank. The respective model involved detailed researches, but finally it could have offered a benchmark for a certain level of the exchange rate. In essence, this model was based on the practical application of the PPP theory in which the retail prices for a selected basket of goods/services from a certain country are compared with the prices of similar products from a developed one, following the model presented in Table 1. This presents, selectively, a few prices of products from Romania as compared with those of similar products from England. The issue was that not all the products from the two selected countries are identical.

In fact, this was and continues to remain one of the key criticism about this theory, namely that correct theoretical foundations are difficult to be computed or justified in practice. The answer to this correct criticism could be offered by the introduction of a new column of the adjustment coefficients within the computation, but such a step implies a high degree of manipulation risk.

Other observations related to the proposed model were and still are regarding the supply and demand of foreign currency (including the level of international reserves and gold), the level of interest rates, consumption habits, traditions, economic structure, level and trends of remittances, etc., all of which are quantified by the model in an indirect way only. All of these are issues which need to be well quantified during the implementation phase of the model. However, in essence, the proposed model is pure and simple a method, but in the case of transition countries any method is preferred to speculative declarations.

Republic of Moldova's Case

The case of Moldova was even more illustrative when it comes to the usefulness of this method. The Moldovan Leu was put in circulation on 29 November 1993 at an exchange rate established by an administrative act at MD lei 3.85/dollar, in accordance with a Decision no. 1 dated 24 November 1993 of the Government of the Republic of Moldova. Based on the good results in the implementation of the reforms, the leu succeeded to remain stable during its first five years from the first circulation at around 4.50 - 4.70 lei/dollar, but the deep financial crisis of 1998 clearly showed that this starting exchange rate was not the equilibrium one.

The leu subsequent developments were under the sign of lack of foreign currency reserves, of much distorted internal prices from the Soviet era and of a structure of the Moldovan economy in which the industrial potential of the country was mainly in Transnistria (being de facto outside the control of the Chisinau authorities). And then the big financial scandals followed (money laundering of the Russian Federation's money through the Moldovan banks, the large financial fraud of one billion dollars, etc.). Under such circumstances, the currency had strongly depreciated up to a maximum level of 24.01 lei/EUR which was recorded on 18 February 2015.

This showed the fragility of a young currency which had to endure the economic and banking conditions, internal and external ones, and which in addition did not have an upfront scientifically computed equilibrium exchange rate. However, over the last two and a half years, the leu has evolved in a stable manner, with some periods of even upward trends, helped by a sound banking policy implemented since April 2016 onwards.

PPP in Simplified Versions

From the above, it was quite clear that while the PPP's theoretical fundaments were not disputed, the practical methodology of implementation has remained unresolved yet. Over the last three decades of transition, many standard products were suggested as representative and useful for the utilisation of the PPP (gas for cars, the simple hen egg, etc.). Under the current context, we believe that the gas for cars is the most adequate standard product, although its pump price is strongly influenced by the tax policy of each country. The current prices for this product confirm the actual exchange rate leu/sterling pound. Meanwhile the economic practice has resorted to a much more simplified instrument, namely to compare the respective prices of another standard product such as the BigMac hamburger sold by McDonald's since 1967 in 36,000 de restaurants in over 100 countries, amongst which the countries in transition as well.

The prestigious magazine The Economist (January 2019) even published an index in this respect, but of course this model is also subject to criticism. For instance, in Russia the hamburger price recently decreased by 15% which is evidently distorting the result of the comparison.

According to this index, the rouble is under-valued against the dollar. More generally, the under-valued currencies tend to appreciate (and vice-versa) during longer periods (some 10 years) in order to reach their equilibrium level, a fact which could be used as a prognosis factor in forecasting the future evolution of a certain currency.

However, on such long intervals of time many exogenous factors could interfere, which make this simplified method even less useful. The more complex model propose above could be updated to the XXI-st century conditions, especially now that the collections of the local prices has become much easier in internet era under which sign we are currently living. Even not perfect, the degree of accuracy of the model is the highest as compared to the other methods and in this case the accuracy represents its most valuable feature.■

Adauga-ţi comentariu